Читать книгу Building the Empire State - Brian Phillips Murphy - Страница 10

ОглавлениеCHAPTER 1

“The Most Dangerous and Effectual Engine of Power”

New York officially became an American city at one o’clock in the afternoon on 25 November 1783. To the sound of pealing bells, Major General Henry Knox and a retinue of horse-mounted dignitaries left Bowling Green, at the foot of Broadway in Manhattan, setting off to the Bull’s Head Tavern on the Bowery, accompanied by a crowd that had assembled at the city’s “Tea-Water Pump” and followed on foot. There they met George Washington, New York governor George Clinton, Chancellor Robert R. Livingston, and other members of a provisional government, which was about to take possession of the southern parts of New York that had been under British occupation for the last seven years.

The thousands of spectators reviewing columns of troops that day were firsthand witnesses to spectacles of regime change reflected even in the naming of New York’s taverns. Evening festivities were hosted at Cape’s Tavern, a site formerly known as the “Province Arms” and then the “City Arms” when it was a favored haunt for the officers of His Majesty’s occupying forces. After being purchased by John Cape, the new proprietor’s first public act was to replace a thirty-year-old sign that had hung above the door with a new one bearing the armorial insignia of the now-independent state of New York.1

However meaningful, the symbolic acts of replacing signs and changing flags were inherently complicated by some unpleasant facts concerning New York City’s population and prospects. With the evacuation of more than twenty-nine thousand British Loyalists complete, there remained just twelve thousand people living inside the belt of Manhattan’s terraqueous border.2 Although people could strip away physical vestiges of British dominion and occupation, the uncomfortable truth was that many of those who remained in the city could be classified as British Loyalists: Tories who had cooperated in the British occupation but who were not so loyal that they felt compelled to leave the United States after the war’s end.

To people like Chancellor Robert Livingston and his circle of correspondents, which included George Washington, foreign affairs minister John Jay, and former New York congressmen Gouverneur Morris and Alexander Hamilton, the presence of those Tories was essential if the city were to rebound as a commercially viable destination for goods and capital. Americans had rejected British imperial governance during the Revolution, but the mercantilist practices and habits of the British Atlantic remained intact and Hamilton in particular was convinced that the new nation needed Tories to help negotiate that world. The willingness of the Tories to participate in American commerce would entangle the city, state, and nation in a web of trade that, both Livingston and Hamilton hoped, would foster geopolitical stability for the United States as a whole. Furthermore, the treatment of those Tories would speak volumes about the intentions and nature of the new American regime and its ability to reconcile with its former kin. And finally, in the view of Livingston’s cohort, New York desperately needed the Tories’ money. The city was hemorrhaging coined metal—gold and silver—that was essential to participate in international trade. There was a real risk that Tories’ capital and connections could be lost for good.

But not everyone was enthusiastic about continuing to host these former Loyalists. During the Revolution, New York legislators punished British collaborators by confiscating their estates and chopping them up to be sold to (ostensibly) patriotic rent-paying tenants.3 Although the war was now over, such punitive acts showed no signs of abating. For months, vitriolic attacks circulated in New York under the “Whig Party” moniker, while selfidentifying Whigs in the legislature stoked their countrymen’s passions by calling for the expulsion of Tories and pressing for invasive new laws to forever bar them from owning property, holding office, or voting, effectively rendering them civically and financially dead. An August 1783 broadside addressed from “Brutus” to the “Tories of New York”—likely penned by Albany county state senator Abraham Yates—delighted in the “remorse, despair and shame cloud[ed] upon [Tories’] imaginations” by fear of American reprisals. “A review of the treason, murder and robberies, which you [Tories] have committed, with a long catalogue of your aggravated offenses against an oppressed but zealous band of patriots,” would follow the war, he predicted. His advice to Tories was to “flee then while it is in your power, for the day is at hand, when, to your confusion and dismay” they would face “just vengeance” from “collected citizens.”4 The day was coming, these Whigs promised, when Loyalists would not be able to hide from the things they had done.

As Yates and his colleagues attempted to foment and channel popular anger against Tories, Robert Livingston chalked their motivations up to greed and self-interest. “We have many people who wish to govern this city,” Livingston told his friend Robert Morris, “and who have acquired influence in turbulent times which they are unwilling to loose in more tranquil seasons.” These legislators had won votes from vengeful and frightened voters, and they wanted to keep those voters vengeful and frightened, even if it meant proposing anti-Tory laws they knew they would never actually adopt into law. The chancellor also believed that Whig legislators were using this veneer of patriotism to enrich themselves. Behind their “violent spirit of persecution,” Livingston told Alexander Hamilton, was a “most sordid interest” in “wish[ing] to possess the house of some wretched Tory” or trying to “engross the trade & manufactures of [New York]” for themselves by driving out a Tory “rival” in “trade or commerce.” Some Whigs wanted to avoid repaying lawful debts owed to Tories, and others wanted to lower real estate values and the “price of Living” by “depopulating the town” of Manhattan. “It is a sad misfortune,” Livingston concluded, “that the more we know of our fellow creatures, the less reason we have to esteem them.”5

But however base these motives might have been, Livingston saw real dangers lurking in New York’s political currents. Calling anti-Tory hostilities a “gathering storm,” he worried that the “smallest spark” might cause the city to “take fire” and overwhelm “all [the] barriers which our weak unsettled government oppose” by transforming rhetoric into riot.6 The city’s “violent papers” were encouraging a “spirit of [Tory] emigration,” observed Hamilton. “Many merchants of second class, characters of no political consequence,” were “carry[ing] away eight or ten thousand guineas” from the “popular frenzy” in New York—a loss of capital he predicted “our state will feel for twenty years at least.7 Writing from Paris to raise alarm with both Livingston and Hamilton, John Jay hoped the “indiscriminate Expulsion and Ruin” of Tories would not come to pass; he reported that “the Tories are almost as much pitied in these Countries, as they are execrated in ours.” “Violences and associations against the Tories pay an ill compliment to Government and impeach our good Faith,” he wrote. Events in New York were being read as a sign of “unnecessary Rigour and unmanly Revenge without a parallel except in the annals of religious Rage in Times of Bigotry and Blindness.” Whigs were “carry[ing] the Matter too far.” Their actions were “impolitic as well as unjustifiable.”8

In the weeks that followed the British evacuation, Robert Livingston, Alexander Hamilton, and a cohort of like-minded, self-styled moderates tried to assuage Whig-Tory tensions in the city of New York by appealing to social ties, crafting legal arguments in favor of revolutionary settlement, and attempting to influence the direction of the city and state’s politics. When those tactics failed, they separately decided that their best chance for success was to found a bank.

In the first three months of 1784, three distinct coalitions began publicly organizing themselves to launch what they hoped would become the first incorporated bank in the state of New York. Each group made it far enough to file petitions with the New York state legislature seeking charters of incorporation. Two of the groups publicly solicited stock subscriptions from investors in advance of those filings. And even after the legislature declined to grant any of their requests for a charter in 1784, one faction went ahead and opened a bank anyway: the Bank of New-York. The directors of that institution persistently filed incorporation petitions throughout the remainder of the decade.

This chapter focuses on illuminating the appeal of incorporated banks at this moment of history in the early American republic. After all, given the avenues open to elite New Yorkers in 1784—from launching a new social club or society to replicating one of the Revolution’s many semi-official committees of notables—why create a bank? And why not simply form a private bank rather than seek state permission for an incorporated one?

On its face, the corporate form is a useful legal instrument that enables a rotating group of people to hold common property over long periods of time and to be a fictitious “person” who could sue and be sued in court as a single entity. But in practice the corporation is a vehicle for the accumulation of capital and influence. The extent of that influence is determined by the underlying purpose and function of the corporation at hand, and a bank’s essential institutional function is to amass capital and offer credit. As institutions that unite human, financial, and political capital under one roof, banks are different from ordinary firms that buy and sell goods. As a route to participation in the Atlantic economy that would reestablish New Yorkers’ access to British and Continental credit, an incorporated bank would present a familiar and reassuring façade to foreign creditors, which would inspire confidence and initiate mutually beneficial transatlantic mercantile alliances.

At the heart of those alliances were transactions; banks could enable them by connecting borrowers with lenders. Yet because a bank’s resources were finite, its directors and managers had no choice but to exercise discretion in deciding who was eligible to gain access to that credit and the institution’s other services. Each time the bank extended itself it was taking a risk; personal relationships therefore were important factors in determining who received credit. Outside the bank’s offices, any person accepting a check drawn on a bank as a substitute for gold coins or paper money had to make a similar set of judgments: about the person passing the check, the name of the person on the check itself, and the bank’s ability to pay that check. Banks, then, were not primarily vaults or even offices. By printing reliable paper money and checks that facilitated the buying and selling of goods and services, they provided a crucial medium of exchange in the local and regional economy. And by lending to borrowers and accepting capital from creditors, banks created institutional networks of obligation and dependence.

For the economically and politically ambitious, no institution in the early American republic offered a more tempting array of advantages than a bank. Bank proprietors and clients were dealmakers and brokers in opportunity, making fortunes for those fortunate enough to be members of its network. The act of granting and tapering access to credit while excluding others from having it is what gives bankers their power; that access was preferential and revocable, enabling bank directors to shower preferred treatment on favored clients, projects, or politics. Banks therefore shape their clients’ interests, and if a bank is a lender to local or state government, its directors calibrate the capabilities and interests of those public entities as well. The existing banks familiar to former British colonists in the late eighteenth century—namely, the Bank of England in London and the Bank of North America in Philadelphia—were quasi-independent arms of the state; no other type of institution was more likely to be regarded with skepticism, suspicion, and outright fear by the public and elected officials alike.9

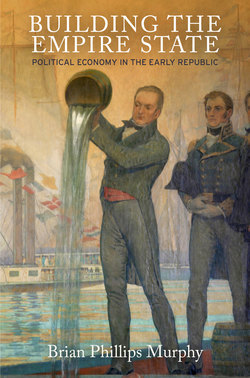

Figure 1. Partly printed check endorsed by Aaron Burr, 24 April 1788. This is an example of an early American bank check issued by the Bank of New-York. Note that because there was only one bank in New York City, the check refers to the Bank of New-York simply as “the Bank” Source: Private collection.

Understanding the utility of banks and the opposition they provoked is crucial to understanding the development of this era’s political economy, but despite the multiple efforts launched to win bank incorporation charters in New York in 1784, the ferocious competition for that prize has all but vanished from modern accounts of this period.10 Histories of early American banking instead tend to settle their gaze on just one of these associations: the Bank of New-York. The reasons are understandable: it was the only one of the proposed banks to open its doors in 1784, it remained the city’s only bank until a branch of the Bank of the United States opened in 1791, and it operated under its own name until a 2007 merger. In addition, the bank has one particularly prominent name tied to its origin story: future Treasury secretary Alexander Hamilton. His role in the bank’s founding and early operations invites observers to view it as an intellectual antecedent of his political and economic philosophy in establishing the first Bank of the United States and a securitized, tradable national debt. Before one can understand Hamilton, the thinking goes, one must study “his” bank.11 Yet the Bank of New-York’s early years—the seven years it operated before it was incorporated—are often ignored in studies of early American finance that rely on quantitative data. The bank did not begin keeping a single set of archived account books or minutes of the meetings of its board of directors until the bank was chartered; therefore, the precise details of its finances remain opaque and unknowable. Approaching the Bank of New-York through Hamilton can be more distorting than illuminating. Hamilton’s position was initially tangential and his influence within the bank was diluted by other directors and shareholders. He owned, after all, just one symbolic share of its stock. Acting as an agent for two wealthy out-of-town merchants, Hamilton had initially planned to help them found their own bank. Once he learned that a coalition had already met to organize a commercially oriented bank, he joined that group and was welcomed by promoters who were as eager to gain access to two large investors as they were to Hamilton’s thoughts on finance. Therefore, studies of New York banks that fixate on Hamilton’s role at the Bank of New-York risk overstating his indispensability and overshadowing the institution’s more authentic originators: New York City merchants and the competition for charters in New York City during the winter and spring of 1784.

The various bank cohorts in New York in 1784 were united by motivations to ameliorate ongoing tensions between New York’s Whigs and Tories by creating a venue for what Robert Livingston called “social intercourse” that would “wear down mutual prejudices.” The bank promoters agreed that anti-Tory politics were blinding both lawmakers and voters to the obvious contributions Tories could make to the city and nation’s commercial and political life, and there seemed to be no easy way to rhetorically persuade political leaders that their long-term self-interest lay in changing course. Moreover, none of the state’s existing institutions had the capacity to offer the favors, privileges, and opportunities that could reorganize the rivalries and contain the animosities threatening to destabilize the infant republic. As he watched the local economy of New York City deteriorate, Robert Livingston ridiculed the lack of money and credit in the city as “republican economics.” Having driven Tories and their capital abroad, the chancellor feared that New York would eventually have to go abroad in search of funds to operate its state government.

Each pro-bank mobilization therefore sought to reach beyond rhetoric by launching an institution capable of offering financial incentives to Tories and Whigs who found common cause with one another, replacing mutual hostilities with transactional trust. Livingston thought a bank would aid New Yorkers in financing their own future and secure the confederation among the new states, “[helping] cement a union that separate [state] debts would weaken.”12 Alexander Hamilton and a group of Manhattan merchants shared similar views regarding the potential for commercial relationships to mend divisions between rival parties. Hamilton proposed that different interests not merely acknowledge mutual ambitions and symbiotic relationships but act on them, too. A bank could fulfill his wish to “make” durable alliances by encouraging Tories and Whigs to “participate” in the “privileges” of the new regime while resetting peacetime trade with Britain.13 The pro-bank activists of 1784 therefore considered commercial and business relationships to be essential features in the civic ecology of a stable and thriving state as well as a union of states. In this way, economic materialism did not merely peacefully coexist alongside democratic political institutions; instead, the two seemed to be fundamentally linked. Business interests tamed the passions and rivalries that deference, aristocracy, and politeness could not master. If the state created the market, the market in turn stabilized the state and gave it the capacity to govern.

Beyond resuscitating the local economy and strengthening the nation’s prestige and power abroad, an incorporated bank would strengthen bank petitioners’ hands in New York State’s political arena. In replacing animosities with alliances, bankers would constrain the ability of New York politicians to continue to exploit anti-Tory sentiment among voters. On a practical level, Tory bank clients would quickly find themselves ensnared in legal contracts and credit relationships, making future legislative assaults more difficult to justify and frustrating to enforce. A Tory-Whig bank would place Tory capital beyond lawmakers’ reach by comingling Tories’ “Loyalist” assets and capital with those of “patriots,” thereby sheltering them from confiscation or seizure. Even as they were being asked for charters of incorporation, therefore, lawmakers were being kept in the dark about one of the true motives behind the pro-bank mobilizations of 1784: an incorporated bank, clothed in the legitimate authority of the state, would become an institutional counterweight to the state legislature. New York officials were being asked to create an institution that would be used to undermine their own governing agenda.

The competing coalitions of 1784 shared another reason for wanting to found a bank in New York: neither the state nor city already had one. Although competition between banks was feared as a potentially destabilizing rivalry, the absence of institutional banking in New York meant that merchants and mechanics alike lacked a stable supply of money and credit, creating logistical challenges for individuals engaged in all kinds of transactions, from buying flour to paying taxes. As Alexander Hamilton argued in a 1783 letter to New York governor George Clinton, without an “incorporation of creditors in the nature of banks” people would be “deprive[d]” of “the benefit of an increased circulation” and would, “of course … [be] disable[d]” from “paying the taxes for want of a sufficient medium.” The consequences were both local and national: a lack of sound money and available credit constrained local commerce and injured the “national faith honor and reputation” of the United States as a whole. “It will be a shocking and indeed an eternal reproach of this country,” he wrote, “if we begin peaceable enjoyment of our independence by a violation of all the principles of honesty & true policy” because of an inability to conduct basic exchanges.14

Yet despite their commonalities, the coalitions who petitioned the New York state legislature for a bank charter in 1784 had inherent differences. Each proposed to serve different interests by prioritizing different functions. The Bank of New-York opened as a money bank, meaning that its paper banknotes were backed by deposits of gold and silver coins called specie. Such a bank principally supported merchants engaged in importing goods to the city, investing in small manufacturing enterprises, and granting credit to each other and a limited circle of dependents. By contrast, the Livingston-backed Bank of the State of New York would be a land bank: its paper banknotes were to be backed with a portfolio of mortgaged lands as well as coins. Such a bank was designed to take advantage of a short-term depression in the city’s real estate market and provide a vehicle for converting existing land holdings into circulating money. Livingston hoped it would become a deposit institution for governments, churches, and charities, enabling the bank to pay regular dividends on its stock and become a profitable investment for its shareholders. Yet it would also inevitably and primarily benefit landowners.

These distinctions are important. By proposing to tether paper banknotes to different forms of collateral, bank petitioners presented lawmakers with a choice about the future direction of the state’s economy. Determining which type of capital—land or coins—was more suitable as a basis for a financial institution’s operations would also determine what interests—landed or mercantile—would gain access to credit in the near future. This choice carried long-term implications for what kinds of economic activities would take root in New York and which professions—landlords or merchants, for example—would make decisions about how to allocate resources and dispense credit in and around the state’s commercial hub of New York City. Therefore, bank coalitions were not simply asking lawmakers to award a bank charter to their favorite interest. Much more was at stake. They were asking the legislators to select a particular kind of bank and—by extension—a particular form of capitalism.

These were weighty options, but they were being laid before New York legislators at a moment when it seemed like lawmakers might welcome a momentous opportunity to shape the state’s future direction by incorporating its first bank. Despite Robert Livingston’s complaint that the state had been stingy in issuing corporate charters, New York City merchants were, in early 1784, already petitioning the state legislature to reintroduce the corporate form to the state’s institutional landscape by reissuing a charter of incorporation to the Chamber of Commerce.15 This move came on the heels of lawmakers intervening in a Whig–Tory dispute among the parishioners of Manhattan’s Trinity Church in late 1783, when the state legislature overturned the election of a Tory rector by opening the church’s 1696 charter of incorporation to vest governing authority in a new state-created board of nine trustees.16 Corporate charters were exceedingly rare in New York in the 1780s, but no more so than in the rest of the nation.17 And although the process of wrangling an act of incorporation from a legislature was no easy task, once state lawmakers had demonstrated their willingness to receive and consider petitions concerning corporate privileges, they created an incentive for new interests to mobilize and lobby for similar benefits. In nearby Philadelphia, some of the city’s wealthiest merchants had recently begun organizing a second bank in their city that would, in the words of Gouverneur Morris, be a “coalition” of “violent Whigs and violent Tories.” Although they had “turned their Backs upon every Body else about two years ago,” these patriots and Loyalists “each performed a Semi Circle and met at the Opposite Point.” New Yorkers need only read their newspapers to learn of these events.18

Therefore, despite the anti-bank and anticorporate suspicions and rhetoric permeating the new nation’s political culture, it was reasonable for New York’s bank promoters in 1784 to think that their state legislature not only could be nudged toward chartering an incorporated bank but also might have actually wanted to receive and approve such a proposal.19 The push for incorporated banks was encouraged by legislators who collaborated with petitioners to define an economy of influence. This helps explain the paradox that emerged in New York City’s (and New York State’s) political economy during the first six months of peaceful American independence: in the immediate aftermath of a revolution waged against monarchy, monopoly, and privilege, New Yorkers saw a stampede in favor of corporations—an imperial vestige that linked all three. Elite merchants and landowners certainly envisioned their proposed corporate banks as mixed-economy public-private institutions that would enable them to gain (and regain) leverage over New York’s official political institutions and policy-making apparatus while profiting from their newfound influence. Yet those proposals also reflected a perceived climate of political opportunity. Livingston, Hamilton, and other political entrepreneurs interwove their business and political strategies to appeal to elected public officials. The corporation was not an unwelcome alien in the early republic; among petitioners and some legislators, it was an invited guest.20

The Land Bank

Robert Livingston was a latecomer to the realization that a corporation—and a bank, specifically—could help him gain financial leverage over New York politics. Initially his plan was to wield power and make profits by speculating in Manhattan real estate. Looking around the city, the chancellor saw prices that he believed were too low and would quickly rebound once the city’s population began to grow.21

Livingston whetted his appetite in late 1783 by buying £2,000 of “good substantial brick houses” that he predicted would bring in £350 of rental income per year. But the estates he truly coveted were far more lavish and ambitious investments. One had recently been the seat of the Loyalist DeLancey family; its current owner, the chancellor suspected, could not afford the home’s upkeep or taxes, and he thought it could be bought for five or six thousand pounds sterling. For Livingston, however, there was a catch: although he was certainly a rich man, he was primarily rich in land. Unless he converted that wealth into credit and cash, he was destined to be little more than a spectator in the real estate boom he was so certain would arrive in the next year.

Livingston’s first instinct was not to seek anything as formal as a corporate charter. He wanted partners with capital, and soon after the British evacuation it seemed Livingston might have found some. Circulating among the merchants trying to mend relations between New York’s Whigs and Tories in late 1783 was Stephen Sayre, a former London sheriff and an ally of the radical journalist and parliamentarian John Wilkes, who supported the American cause during the war. Sayre once ran a private bank in London and had returned to Manhattan—his birthplace—in the fall of 1783 seeking to make a new fortune. There he began attending the Whig-Tory “dancing assemblies,” where he met Major General Henry Knox, Chancellor Livingston, and Livingston’s brother-in-law John Stevens, a merchant. Sayre also resumed a past friendship with Isaac Sears, a longtime member of the New York City Chamber of Commerce. Sayre and Livingston quickly began using these social events as they were intended to be used: as venues to generate business relationships that would sow political reconciliation and reinvigorate commerce. They recruited Stevens and Sears to be their partners in real estate speculation.22

According to Livingston, Sayre first proposed that the cadre broker a Dutch loan that would enable New York’s state government to help repay its war debts. At the time, Sayre claimed to have good contacts in Holland but not in New York; therefore, he needed Livingston, Stevens, and Sears to exercise their influence with decision makers in the state and city to make a Dutch loan palatable at home. If the partners could collect fees and commissions for marketing and handling the transaction, Sayre suggested, they could use those proceeds to build the real estate portfolio Livingston had been eyeing.

Chancellor Livingston was never enthusiastic about this plan, and “discouraged” Sayre from pursuing it any further. Livingston did not want New York, or any state, to “contract a foreign debt independent” of the money “borrowed [abroad] by the United States.” Congress’s national debts, he explained, “help[ed] cement a union that separate [state] debts would weaken.” Livingston was therefore unwilling to put profits ahead of principles if it meant jeopardizing the union that existed among the new states.23

In response, Sayre pitched a second idea: why not simply use a Dutch line of credit to make “loan[s] to individuals on real property”? This plan would appeal to Livingston, who was eager to see his vast land holdings become a source of ready, liquid money; it would provide him with cash and make him a patron who could offer credit to others.

Livingston liked the idea. However, he also seemed to believe that his aristocratic name alone could open doors and opportunities that were off limits to others. Before committing himself to support Sayre’s initiative, the chancellor wanted to find out for himself whether Sayre’s Dutch contacts would find it acceptable. He also wanted to see if he could go behind the backs of his partners to carve out a more lucrative side deal for himself. So he wrote to the Dutch minister to the United States, Peter J. Van Berckel, to find out whether he “approved or disapproved” of a credit-for-land idea. He explained to Van Berckel that “in every monied transaction” he preferred to “deal with the Lenders himself than (by a Broker) thru a third person.”

Livingston plainly hoped that he could enlist Van Berckel to use his influence at home and abroad, swaying Dutch investors to support a landinvestment plan and structure their loan in a way that would make Livingston the leading partner by displacing Stephen Sayre. To the Dutch minister, Livingston offered unequivocal support for the propriety and profitability of land investments. The departure of Tories who had “quited the state,” he said, combined with the “little command that any persons among us have of money,” had “opened a large field” for investments in real estate. He predicted that before “ten or twelve months or the restoration of commerce & the arrival of strangers” in New York City, these land purchases could “make immediately” an 8 or even 10 percent profit.

Livingston saw himself buying and selling these properties, he told Van Berckel, rather than working with partners and splitting commissions as he would have to under Sayre’s proposal. He hoped the minister and his “friends” would “think the interest I offer sufficient to enduce you to lend your money … draw[ing] bills upon England or Holland” to “put into my hands;” it would then “be vested in real property.” Offering that he was “not nor ever was engaged in trade” as a merchant and that his “property consists of … land and houses as I live within my income,” Livingston even assured Van Berckel that he would offer a personal bond as security for a Dutch loan of £6,000. “It is impossible,” he boasted, “for any person to offer better securities than I can.” Moreover, if the minister personally became an investor, Livingston could advance him funds for a shared “joint account” that he would personally manage on Van Berckel’s behalf.24

This was a bold and an underhanded offer on Livingston’s part. And he knew that if his letter were shared, its contents would be toxic both to his reputation and to the opportunities at hand. Livingston not only would be betraying his partners but also would be putting their entire scheme at risk by tipping off other investors about gains to be made in New York. Moreover, if Van Berckel shared the letter’s contents, the chancellor feared that people in Philadelphia might initiate “speculations that serve to empower enemies.”

“Enemies” might seem a hyperbolic term to use in the context of real estate speculation, but Livingston was not referring to business rivalries or the scandal of being exposed as a double-dealing partner. Rather, he was worried that faraway Philadelphia investors could “empower” already mobilized factions of mutually suspicious Tories and Whigs in New York City. Thus there would be no better way to “empower enemies” in New York than by revealing that there were large profits to be made from the purchase and sale of Tory estates. Should they learn that out-of-state and foreign investors were pooling their capital to take advantage of the state’s real estate market, New York lawmakers might be tempted to intensify anti-Tory hostilities and adopt even more aggressive laws to punish Tories and seize their property, violating the spirit and letter of the peace treaty between Britain and the United States and upending the revolutionary settlement that Livingston, Jay, and other moderate Whigs hoped to achieve.25

Making matters even more potentially explosive, Livingston was seeking British credit to finance his plans. The chancellor had asked John Jay to “establish … a credit for me upon some good house (either in England or Holland)” that could be used by him and his partners, who were likely spending their time casting about in London, Liverpool, and Amsterdam in search of credit as well. Therefore, as they conspired to profit from anti-Tory hostilities and expulsions by speculating in real estate that had been seized from or abandoned by Tories, they were looking to make those purchases with foreign—and even British—credit. No wonder Livingston feared that “hotheaded” Whigs would paint him and his associates as “suspected.” If anyone found out about his partners’ plans and his own personal duplicity, his credibility could be devastated.26 As reckless as these actions might seem, Robert Livingston took them as a man of sound mind. He was a political entrepreneur and an aristocrat operating in New York during the immediate months that followed the end of the Revolution—a man who felt at liberty to conduct business as he saw fit, negotiating and negating agreements that privately contradicted his public statements. Perhaps because he did not feel that Stephen Sayre was one of his peers, Livingston considered their arrangements to be provisional. He saw himself as a man without boundaries.

Yet Livingston was about to learn that both his name and the pre-Revolutionary habits and impulses with which he had been raised would prove to be insufficient in helping him successfully navigate the political economy of post-Revolutionary New York. Only days after sending his letter to Peter Van Berckel, Livingston received a reply. In it, the Dutch minister declined his request for credit. He simply did not have “time enough to write to my friends” in Amsterdam right then. Then Van Berckel revealed that he could not partner with Livingston since he had already “thought it prudent to join with gentlemen” who were pursuing a similar scheme to invest in Toryowned New York properties. They included Gouverneur Morris, New York land baron Philip Van Rensselaer, and Robert Morris. These men, the minister explained, had “experience and knowledge” and his “engagement” with them “put out of any power to do for another what I want to do for myself.” Van Berckel closed his letter by suggesting that Livingston lift his request for silence; he wanted to know if the chancellor would be willing to join with them to everyone’s “mutual advantage.”27 In reply, Livingston had no choice but to grudgingly “congratulate” Peter Van Berckel for making allies with men of “judgment & integrity.” He hoped, however, that their “objects may not be the same” as his, and steered them away from “this Island” of Manhattan toward “improved and unimproved Land in other parts of the State.”28 Thus it turned out that Livingston would need his partners after all. Without credit from Van Berckel or Jay, he also needed a new plan.

It was at this moment that Livingston decided to try to become a banker. A corporation offered the institutional advantage of installing himself and his partners at the center of their real estate speculations, and an incorporated bank—particularly a land bank—would enable him to raise outside investment capital and convert his personal land holdings into cash.

Although Livingston’s shift of priority from real estate speculation to bank proprietorship had taken place in just under two weeks and smacked of pragmatic opportunism, it nevertheless forced him to recalibrate both his goals and his stated agenda. When dealing solely with private partners, the chancellor had mainly expressed interest in the private profits to be had in real estate speculation. But once he began pressing for a bank charter, Livingston began highlighting the civic benefits such an institution could deliver to the city and state.

Newspaper advertisements placed in the 12 February 1784 editions of the New York Independent Gazette and the New York Packet claimed that the land bank would be both a “place of safety for cash” and a tool that “renders aid to merchant and tradesman.” Livingston and his partners pointed to Venice, Amsterdam, London, and even Philadelphia in its “infancy” as places where “great profits” had rewarded the “proprietors” of banks and “supported and created a system of credit extremely advantageous to … trade and revenues.” They suggested the bank could reconcile Whigs and Tories by tying the two groups together through business relationships and pushing back against aggressive anti-Tory legislators. It was “universally acknowledged,” they claimed, that there were “great benefits to commerce and society at large, to be derived from well regulated BANKS, especially in republican governments, where the hand of arbitrary power is restrained by law.” In addition, banks created order in commerce and society by “compelling society to punctuality in contracts,” enabling people to “make fresh ones.” They made it possible to do “more business in less time and with greater facility.”29

These public statements about banking were not about profits; they offered a prospectus of civic benefits, reflecting an awareness that the public good would have to be served by the state’s first incorporated bank. Livingston, the consummate political operator and entrepreneur, simply did not feel that it was appropriate to seek a corporate charter to serve his private ambitions. There was something inherently transactional about applying to the state legislature for a bank charter. Even Robert Livingston felt that it was appropriate to place the public character of that institution at the center of his mobilization efforts. As an institutional extension of the state, a bank would be an agent of regulation, making commerce orderly, monitored, and efficient. And as an institution operating within the apparatus of the state, a bank could act as a safeguard against abusive legislators. In this vision, there was no conflict between incorporated banking and the flowering of a democratic republic; banking, in fact, promised to stabilize the regime. Incorporated banking was therefore being sold to the investing public as a commercial activity that had an inherently political character, and bank directors would be individuals who would wield both political and financial power within the early republic’s economy of influence. For these reasons, the Livingston-backed proposal was to be called the “Bank of the State of New York,” soliciting investments from an office at No. 6 Wall Street.

According to published details, the bank was to be managed by six directors who would be elected once the bank recruited its first 300 subscribers.30 One thousand shares would be available for purchase; each was to cost $750, with one-third of that paid in cash and the remainder pledged in “landed security”—mortgaged properties in New York or New Jersey that would be credited for two-thirds of their assessed value. Shareholders would be allowed to borrow money from the bank, up to one-third of the assessed value of the lands they mortgaged. The bank would therefore enable land-owners to transform their properties into circulating, liquid money. All told, the bank’s credit would be based on assets worth $1 million: $250,000 in gold and silver specie and $750,000 in mortgaged land titles. The bank promoters knew this investment would present risks to shareholders, but they promised that investors’ other assets would be shielded in the event of the bank’s failure; no subscriber was “liable for debts beyond his stock.” Moreover, no salaries would be paid to the directors or clerks of the bank until shareholders were first paid a dividend.

To observers, it should have been obvious from the 12 February newspaper advertisements that the land-bank proprietors intended to forge a formal relationship with the New York state government. By describing the bank’s potential to serve a public good as one that depended on them being “well regulated … especially in republican governments,” the promoters anticipated that state lawmakers would eventually be forced to author a set of legal rules to govern and guide its operations. Of course, the bank’s directors would presumably wield a heavy hand in shaping such regulations. Once codified in state law, the Bank of the State of New York would then become an institution designed to not only reflect the interests of the state’s largest landholders and specie-rich merchants; it would also formally structure that interest, consolidating its membership into a corporate institution that—with shares priced at $750 apiece—would speak in the voice of its wealthiest owners.

From the start, then, it was understood that the land bank was not an apolitical entity that spontaneously sprang forth from the private marketplace; instead, it was an institution that deliberately mixed interests—landed and mercantile, established aristocrats and nouveau riche arrivistes, and private citizens along with office-holding public servants—to stockpile financial as well as political capital. And there, from atop the perch of one of the only incorporated banks in the western hemisphere, Robert Livingston and his partners would be able to influence the hearts and minds of the state and nation’s top policy makers by dispensing a much-desired but limited commodity: access to credit.31

But as they read the plans for the land bank, New York City merchants began to appreciate just how much the land bank would privilege the interests of landowners over others. Land-bank shares would have to be purchased in part with mortgaged lands, therefore merchants who did not own real estate would be ineligible to buy shares unless they first bought property to mortgage at the bank.

Here is how the math would work out:

One share would cost $750. Because an account would be credited with two-thirds of a mortgage’s face value, a $750 land purchase would be worth $500 at the bank. A merchant would therefore have to top off that sum with $250 in coined money. Not including transaction costs—legal fees, commissions, appraisals, taxes, and surveys—it would therefore cost a merchant at least $1,000 in cash and property purchases to buy a bank share worth only $750.

By comparison, someone who was already a landowner would need to raise only $250 in cash to purchase that same bank share after mortgaging his or her existing holdings at the bank.

Thus, an inequity had been structured into the land bank’s design: one that privileged property holders over coin holders. This distinction would be even more magnified among the bank’s directors, who had to own four shares of stock. Although Robert Livingston would meet that requirement with only $1,000 coming out of pocket, a city merchant—someone like Isaac Sears, one of Livingston’s and Sayre’s original partners—would have to spend $4,000 to buy the same number of shares. Yet as equal shareholders on paper, both men would be eligible for the same amount of bank credit. What merchant would trade $4,000 in gold and silver coins for the same face value in less secure paper money?

The proposed Bank of the State of New York would therefore be incapable of answering the commercial credit needs of either the city’s merchants or their customers. Paper notes backed by land instead of gold or silver coins would never pass muster among merchants who were accepting only two sources of domestic paper money at the time, both of which happened to be from Philadelphia: those from the Bank of North America and so-called Financier’s Notes issued by Congress’s finance superintendent Robert Morris.32 City merchants came to view Livingston and Sayre’s proposal as fundamentally flawed—not because it was a land bank, but because it was designed primarily to serve landowners.

The Private Bank

When Alexander Hamilton first heard that people were proposing to open a land bank in New York City, he believed it had been the brainchild of Stephen Sayre. Later, he would say that he had always known the “true father” was Chancellor Robert Livingston.33 Either way, Hamilton was under instructions to not pay too much attention—a directive that had come from John B. Church, the wealthy British merchant who in 1783 had hired Hamilton to be his agent in America.

Although Hamilton was a relative newcomer to the city, his experience made him well suited to succeed in its commercial affairs. He had worked as a clerk in a St. Croix import-export house after being orphaned in 1768 and had run the firm’s headquarters for several months in 1771 when he was just sixteen years old. He therefore knew how to contract debt, pass bills of exchange, and negotiate transactions, making him intimately familiar with the skills needed to run the portfolio of a successful trading firm.

In the early 1780s, Hamilton befriended two men who made a fortune during the Revolution: John B. Church and the merchant Jeremiah Wadsworth. When the duo left American shores for Paris after the war to buy goods and collect debts, they made Hamilton their go-to man in New York City. Being Church’s agent meant that Hamilton was charged with managing his business affairs, investing his funds, and acting as his legal representative. It also meant that he had a breathtaking amount of daily autonomy; in the fall of 1783, neither Hamilton nor John Chaloner, who, as Wadsworth’s top American agent in Philadelphia, was Hamilton’s counterpart, had heard from either of their principals since July.34

Being Church and Wadsworth’s agent also meant that, by late 1783, Hamilton was already thinking like a banker. Church and Wadsworth, after all, were no ordinary merchants. Among their many assets was the largest single bloc of shares in the Philadelphia-based Bank of North America, then the only bank in the nation. Hamilton was in charge of Church’s half, managing a combined investment of 202 shares worth just under $82,000. He was directly responsible for collecting dividends paid on Church’s bloc of shares and held a power-of-attorney that entitled him to cast shareholder votes in Church’s name, making him the proxy voice for one of the country’s most important merchant-bankers and a de facto stockholder in the bank itself.35

Despite all their influence within the Bank of North America, however, Church and Wadsworth were unhappy with how the institution was being managed. They suspected that bank president Thomas Willing was collaborating too closely with his onetime business partner Robert Morris, the financier and merchant who had been Congress’s superintendent of finance since 1781. When Willing announced in December 1783 that the bank was expanding and would put additional stock shares up for sale, it looked to Hamilton like Robert Morris was behind that plan, one that would cost his clients money and dilute their influence within the bank. Chaloner predicted the new stock would “lessen the dividend” paid to current shareholders—reducing the profitability of bank shares as an investment—and “throw it out of the power of a few individuals” to select directors and “control” the bank itself.36

Moments like this tested principal-agent relationships in the eighteenth century because the physical distance separating Hamilton from Church could be narrowed only by trust. Although Hamilton wrote to Church for instructions in December, his letter did not reach London until February. Church’s response, penned days later, did not reach New York until later in the spring. He and Wadsworth directed Hamilton to discreetly “strain at every nerve” to buy up the new shares in the Bank of North America.37

But during the intervening weeks when letters were in transit, Hamilton’s on-site autonomy and judgment led him to begin working on a different plan. In his December letter, Hamilton suggested to Church and Wadsworth that instead of tangling with Robert Morris and fighting a corporate structure rigged against them in Philadelphia, the partners should open a bank of their own in New York City. Such a bank would be unincorporated and have no shareholders. The only people with equity in the venture would be Wadsworth and Church; although this meant the bank would be smaller than the Bank of North America, the advantage would be that nobody else would have a say in its governance or management. The bank Hamilton offered to help set up would therefore be the partners’ own private commercial bank—their own personal “engine” of regulation and power in New York City.38

Church and Wadsworth envisioned their bank as an avenue to extract profits and deploy leverage in New York, and to maximize this effort they intended to restrict ownership in the bank solely to themselves. Therefore, when Stephen Sayre approached Alexander Hamilton in late 1783 to solicit Hamilton’s principals to join the land bank he would soon propose, Hamilton refused. Moreover, he did not tell Sayre that Church and Wadsworth were already nursing bank ambitions of their own. Recalling the encounter to Church, Hamilton seemed to not realize that Robert Livingston had partnered with Sayre; Church dismissively said he would be “sorry if Mr. Sayre should effect his Establishment” but “astonish[e]d if Men of Property are weak and credulous enough to give him their Confidence.”39

What Hamilton and Church did not yet realize was that those “Men of Property” would soon not need to have confidence in Sayre alone. Once Chancellor Robert Livingston and merchant John Stevens became the highly visible front men for the proposed land bank, they were the authentic men of property threatening Church and Hamilton’s plans.

In response, Hamilton spent much of February working to “start an opposition” to what he called the “scheme” of the proposed land bank. There was “great reason,” he believed, to fear that the legislature would approve the land bankers’ request for both a corporate charter and a law declaring it exclusive, which would prevent competing banks from being incorporated. “For the sake of the commercial interests of the state,” Hamilton was making it his mission to “point out [the land bank’s] absurdity and inconvenience to some of the most intelligent Merchants,” some of whom eventually “saw the matter in a proper light” and joined in opposition.40

Hamilton also began a whispering campaign to “convince the [land bank] projectors themselves of the impracticability of their scheme.” In this he was aided by the land-bank promoters after they raised doubts about the propriety of mortgage-backed paper money, asking if buildings could be accepted as collateral if they were not insured against the risk of fire. On 16 February—one day before their incorporation petition reached the state assembly—Livingston or one of his partners answered their own question by announcing that “some Gentlemen have it in contemplation” to form a fire-insurance company and that once “such houses … are insured, [they] will be of course, received as security in the Bank.”41 This statement must have shaken confidence in the land bank’s backers, sparking investors’ imaginations to begin asking what other risks awaited them besides fire? The land bankers had clearly not thought through the consequences of their plans and had now committed to founding and managing not one but two new institutions in the city: a bank and an insurance company.42

Yet even as support for a land bank eroded in New York City, its prospects nonetheless seemed robust in the state capital. According to Hamilton, Robert Livingston “had taken so much pains” to cultivate support among landowning legislators—Hamilton called them “the country members”—that he feared they were coming to see the land bank as “the true Philosophers stone that was to turn their rocks and trees into gold.”

Hamilton decided he had to block the land bank once and for all, and as he peeled away supporters he hoped he could convince them to rally around the bank he hoped to found on behalf of Church and Wadsworth, who were prepared to sell their Philadelphia bank shares and reinvest the profits in New York.43

The Commercial Bank

Up to this point in February 1784, the one group with the most at stake in Manhattan’s bank machinations had been sidelined: the city’s merchants.

From the periphery, they watched as would-be land bankers sketched an institution incapable of meeting their credit and commercial needs while seeking an exclusive charter of incorporation from the state legislature. At the same time, they learned that Alexander Hamilton’s elite patrons were planning to open a private bank, subjecting the whole of their community to the whims and wills of two faraway and well-connected competitors. The former threatened to place landed aristocrats at the head of the state’s first and only bank; the latter would give John B. Church and Jeremiah Wadsworth a unique capacity to distort New York’s political economy. In response to these prospects, New York City’s mercantile community began countermobilizing by drawing up their own plan for a bank. Of the three proposals, theirs would be the only bank to actually open (and survive to the present day): the Bank of New-York.

The first public sign of the merchants’ organized resistance appeared in the 23 February edition of the New York Packet. A letter from “A Merchant” announced that a proposal would soon be “delivered … for the establishment of a Bank on the most equitable and generous footing” to be called “the Monied Bank of New-York.” The writer then turned to dissecting the flaws in the proposed land bank. Although he agreed with the land bankers’ claims that banks in general could deliver “great benefits,” he believed that “success … depend[ed] on the nature of [its] foundation.” The Livingston-backed land bank was flawed, he explained, because it was “clearly founded” to “[add] consequence to the landed interest” in New York. “The language” of Livingston’s prospectus assumed that “commerce is dependent on agriculture” and therefore proceeded as if “the landed interest must be of more consequence to the society than the commercial.” In the writer’s view, however, that “idea is absurd.” Holland, after all, needed “no landed interest to support her.” Instead it was “commerce, the first spring of the whole machine,” that found a market for “the fruits of agriculture.”

In addition, the writer alleged that the land bank had been designed to benefit particular landholders, including Robert Livingston. He believed that even before its subscription books were officially opened to the public, the land bank’s board—“its Governor, Directors, and Cashier”—were “already in nomination.” He had been told, he reported, “one gentleman has been induced to subscribe to four shares, as he is intended for a director.” The mercantile letter writer hoped the land bankers’ petition would “meet with the fate it merits,” because “free people” had no need to show “such partiality,” particularly when no “thing was known before in a Free Country.” Even the Bank of England, “that source of wealth,” did not have “an exclusive privilege,” and the “resentment of the Public will not be less than their surprize” if the New York legislature granted Livingston’s request for an exclusive charter of incorporation—one that would not only establish the land bank as a corporation but also bar any other bank promoters from receiving a corporate charter for years or even decades to come. A more equitable alternative, the “Merchant” promised, would materialize “shortly.”44

Three days later, on 26 February, retired major general and current state senator Alexander McDougall presided over a meeting at the Merchants Coffee-House where “merchants and citizens … unanimously” vowed to form a bank of their own. The “Bank of New-York,” as it was to be called, would be a money, or commercial, bank with paper banknotes backed by gold and silver coins. The bank would make short-term loans called discounts at a 6 percent interest rate. There would be one thousand shares of stock for sale, priced at $500 each—half of what land-bank shares would cost a merchant. Shareholders would be expected to pay the first half of their stock subscription at the bank’s first meeting; they would have to pay the second half six months before being eligible to receive the bank’s promised twice-yearly dividends. The bank’s officers—a president, twelve directors, and a cashier—would be chosen by a plurality of votes cast by shareholders in elections designed to favor smaller investors. Each shareholder would receive one vote per share for their first four shares, shareholders with six shares would command five votes, those with eight would have six, and those with ten or more could cast seven. Therefore, no shareholder could cast more than seven votes no matter how large their investment. With a twelve-member board of directors (twice as many as the land bank), an electoral system that maximized the influence of smaller investors, and a set interest rate, the bank’s structure explicitly discouraged the hoarding of shares by people trying to take over the institution or seek special, more favorable borrowing terms.45

In these ways, the Bank of New-York was designed to answer the perceived financial flaws in the proposed land bank and the elite dominance of the Church-Wadsworth private commercial bank. Although any bank that backed its paper with specie would naturally be more oriented toward mercantile interests, the Bank of New-York promised credit to a wider community of less wealthy, newly established merchants than those who dominated the city’s older transatlantic trading houses. Each of the six men who co-signed the advertisement announcing the bank’s details were “merchants,” a label that seems superficial when one considers the varieties of political experience they brought to bear in making their proposal. Most had held public office in the provisional state government or had served on local committees during the Revolution; one was a sitting city alderman. A person who wanted to subscribe for Bank of New-York stock would have a choice to do so at John Alsop’s law office, Robert Bowne’s printing and stationery shop, or Nicholas Low’s mercantile firm. On the whole, these promoters were younger, more directly engaged in politics, and less economically secure than many of their social and economic betters, also called “merchants”; only one of the six was established enough to have been a member of the city’s Chamber of Commerce before the war—the remaining five were still climbing toward that status. The Bank of New-York was therefore a political mobilization led by political entrepreneurs seeking state support for a financial institution capable of representing the interests of a broad spectrum of the city’s commercial sector.

Two interests of that commercial sector in Manhattan were Tory-Whig reconciliation and revolutionary settlement. The bank supporters’ selection of Alexander McDougall as their nominal leader was meaningful on this front. He had been one of the most radical merchants in the state before war, and now at the age of fifty-two was one of the city’s senior statesmen and its current state senator. McDougall therefore had political clout. More important, he had been one of the foremost advocates for postwar reconciliation in the city.

When elections were held in the fall of 1783 to choose the members of a provisional state-level government that would transition the city from British occupation to American independence, a broadside was printed to target the city’s working-class mechanics—among them, blacksmiths, silversmiths, and hatters. The author, using the name “Cincinnatus,” had cautioned that a hostile climate for Tories would ricochet back on the people creating it, injuring their own commercial and financial prospects and sowing chaos. “The[se] [Tory] families,” Cincinnatus warned, “will go to neighbouring states, and we can expect none to come amongst us, but adventurers who delight more in tumult and anarchy, than in order and good government.” Envisioning a distinctly urban collaboration between laboring mechanics and commercial merchants, the author of the broadside urged mechanics to vote for merchants in special legislative elections to be held several weeks in the future. In London, “the largest and richest city in Europe, made so by Commerce,” voters had “chosen for her Representatives, Merchants, men well versed in the practical knowledge of trade.” New Yorkers, Cincinnatus concluded, would be wise to follow suit by remembering that their city was no island. “Our local situation, on what the city of New-York has to rely, not only for her own existence but for that of the adjacent country” could be succinctly summarized “in one word,” he wrote, before plainly declaring: “It is Commerce.” The broadside was not an empty call for unity; rather, the author wanted mechanics to temporarily set aside dissatisfactions they had with merchants just long enough to elect them to office.46

Given the nom de plume “Cincinnatus,” the broadside’s author was probably Alexander McDougall. His plea, however, met with fierce dissent. One reply authored by “a battered soldier” shouted that, of all the groups in the city, merchants were the least patriotic or fit for office. Candidates “who profess themselves to be your Friends” and were “of good natured Dispositions” were plainly too ambitious to be trusted. Moreover, merchants had shown themselves to be too forgiving of Loyalists’ misdeeds. “From their natural Timidity, Want of Firmness, and [the] intimate Connexions, by the Ties of Consanguinity, or Marriage” to Tories, the writer warned, merchants would naturally “feel disposed to pardon the most obnoxious Tories.” “If you [mechanics] fail” to elect candidates who will firmly punish Tories, he predicted that “you may depend on it that you and your Children will soon become Hewers of Wood, and Drawers of Water, to the Tories in this State.” In other words, either the Tories had to be defeated or the state’s patriots would once again find themselves under British domination.47

Consolidating Forces

Alexander Hamilton did not attend the first meeting to organize the Bank of New-York. In steering Manhattan merchants away from the land bank, he had hoped to drive them into the arms of a Church–Wadsworth bank, but they showed little desire to trade one form of financial domination for another. Hamilton knew, moreover, that it would become harder to establish a bank for Church and Wadsworth once the Bank of New-York was organized. The shares, he explained to John Church, had “been taken up by the broad footing of the whole body of the Merchants” in the city. Under those circumstances, he continued, “it never would be your interest to persue a distinct project in opposition to theirs.” Though it “embarrassed” him, Hamilton therefore “concluded it best to fall in with” the Bank of New-York before it was too late. By “employ[ing] [Church and Wadsworth’s] money” to make them “purchaser[s] in the general bank,” Hamilton hoped “to induce” the bank promoters “to put the business upon … a footing” that would “enable” Church and Wadsworth “[to combine] interests with theirs.”48

The bank’s promoters were more than willing to accept Hamilton’s involvement in their institution. Even though he had no fortune of his own and would never own more than one symbolic share of the bank’s stock, Hamilton’s name was added to the would-be board of directors.49 In conversations with the bank’s “most influential characters,” Hamilton set about convincing them to relax their restrictions on shareholder voting. Originally, he explained, “no stockholder” of “whatever amount” could cast “more than seven votes.” But Hamilton convinced them to allow shareholders one additional vote for every five shares they owned in excess of ten. This, he reported to Church, was as far as the Bank of New-York’s promoters would “depart” from their original limits. The change, however, gave Church and Wadsworth a greater voice within the institution and how it distributed credit. Therefore, even before the “Constitution for the said Bank” was drafted, Hamilton had made substantive changes to the institution’s design.

Although Hamilton is often credited with being the bank constitution’s author, the true extent of his contributions is unclear; the copy of the document found in his files was not in his own hand. It does, however, bear his intellectual fingerprints: subtle but substantial alterations to strengthen shareholder governance and security beyond what was outlined in the bank’s original plan. These changes included adding one more seat to the board of directors to make it a tie-proof cabinet of thirteen, which would, in future elections, directly choose bank officers by majority votes. The new compact empowered directors to expand the bank’s capital and required them to take oaths of office before a city magistrate. And perhaps most important, a provision in the constitution’s nineteenth article mandated that the president and directors apply to the New York legislature for a charter of incorporation and file separate petitions seeking laws that would make “Fraud or Embezzlement” a crime and “punish the Counterfeiters of Bank Notes and Checks” as they thought “necessary and proper for the Security of the Stockholders and the Public.”50 This was not to be a bank that existed separately from the state. Rather, it depended on government for corporate privileges and statutory regulations that would allow it to function more effectively in the marketplace. The bank was asking the state for recognition and inviting it to expand its involvement in the local and regional economy by regulating transactions and banking activities.

Similarly, Robert Livingston’s outline for the Bank of the State of New York had called for state “officers of the government” to “inspect [the bank’s] books” and “examine their mortgages,” in exchange for the bank serving as the “receptacle of public money” and having its “notes taken in taxes.” In other words, the bank would welcome the intrusion of inspection if it was granted the privilege of being the official state bank and the repository of public funds.51 New York’s bank promoters therefore not only knew that the state legislature would be involved in their institution if they were granted a charter, they were counting on it; state-imposed regulations would be a necessity, as would the drafting of new laws to define and protect the bank’s operations. These expansions of state power were explicitly sought by bank promoters.52

The Bank of New-York’s petition was submitted to New York lawmakers on 12 March—three days before a shareholder meeting “officially” ordered them sent. Nearly a month had passed since Robert Livingston and the landbank proprietors had submitted a petition for the exclusive incorporation of their institution. A state assembly committee had already drafted legislation to charter the land bank and give it exclusive privileges for two years, a law that would have prevented any rival banks from opening in the state during that time. The Bank of New-York’s promoters therefore not only had to win a privilege for themselves; they also had to defeat a legislative process already underway.53

Former Sons of Liberty leader and merchant Jacobus Van Zandt—an advocate of specie-based money and a speculator in Tory-forfeited lands—was the first signer of record on the bank’s petition. Conveniently, his nephew Peter P. Van Zandt was a newly elected member of the state assembly from New York City.54 There were other connections, too, as Alexander McDougall was a leader in the Bank of New-York and a state senator, and Isaac Roosevelt was a city merchant and one of the bank’s newly chosen directors. With the exception of Alexander Hamilton, the new board of directors was composed entirely of merchants. Bank president Alexander McDougall, more than any merchant in the state, had unassailable patriotic credentials. Two other directors—Thomas Randall and Comfort Sands—were merchants who had tried to run for political office in the recent past and had been opposed by the city’s more working-class mechanics.

Yet these figures were far less controversial than three other men in the group: onetime Loyalists Joshua Waddington and Daniel McCormack, both of whom were bank directors, and William Seton, another Loyalist who was to be the new bank’s cashier, conducting its day-to-day affairs. The new bank seemed to have become a vehicle for urban coalition building among Whigs and Tories, garnering its support from former Loyalists, subtle varietals of “hotheaded” and moderate Whigs, established merchants and ambitious upstarts, onetime land-bank supporters, and even some of the city’s mechanics.55

The capacity to create common interests among onetime enemies and potential rivals had been one of the Bank of New-York’s earliest and most important assets, making converts among those who might have otherwise opposed it more forcefully. Alexander Hamilton, for example, might not have wanted to undermine this burgeoning coalition in Manhattan, knowing that in Philadelphia a new bank had become a “coalition bank” composed of once-“violent Whigs” and “violent Tories.”56 Land-bank supporters, too, recognized that the Bank of New-York—more so than their own proposed bank—was an effective tool to advance Tory-Whig cooperation. Even Robert Livingston’s brother-in-law Thomas Tillotson acknowledged as much when, after critiquing anti-Tory legislation, he reassured Livingston, “I wish you to understand that I mean not to adopt Genl. McDougal[l]’s plan, but mean that they should get [Senator Abraham Yates] out of the Senate.” Tillotson therefore viewed the Bank of New-York and Alexander McDougall’s leadership of it as evidence of its potential to advance Tory-Whig reconciliation and to frustrate Yates.57

In their harshest critiques aimed at each other, advocates of both the land and money banks hesitated to openly question the loyalty or motives of their rivals; public letters that can be traced back to the banks’ promoters during the first months of 1784 focus almost exclusively on the merits of their respective proposals, suggesting that these were not rhetorical attacks but efforts to persuade. The land- and money-bank coalitions each believed their charter applications would be strengthened if they could expand their appeal by attracting supporters and investors from the rival cohort or by offering concessions that would consolidate the two proposed institutions into a single pro-bank effort. Even though Alexander Hamilton thought the land bank was “a wild and impracticable scheme” and had worked to array “all the mercantile and monied influence … against it,” he did not take to the city’s newspapers to attack Livingston and his allies.58 Instead, he directly solicited the land bankers’ support by carving out room for their interests within the Bank of New-York. According to notes kept by Hamilton concerning the bank’s charter application, he and his colleagues considered allowing one-fifth of their bank’s capital—up to $200,000—to consist of mortgaged properties.59

Robert Livingston’s critiques were tempered by a reluctance to have the land bank seen as a divisive counterweight to the Bank of New-York. He rejected the claim that “a monied interest and a landed interest of Merchants and Farmers” were necessarily “opposed to each other, when common sense must dictate that they are members of the same body, and mutually support each other.” “The Merchant” he stressed, “could not exist without the Farmer, and the Farmer without the Merchant would be a dissocial solitary animal.”60 Livingston acknowledged that the land bank could be more solicitous of “monied persons” in the future and lauded Alexander Hamilton for “sh[owing] what appears to me faulty in the constitution of the Land Bank.” The quality of mortgaged lands could be improved, he conceded, and it was unfair to ask merchants to “[draw] too much of their stock from trade to vest it in lands” in order to buy shares in the land bank.61 Livingston, therefore, exhaustively highlighted the advantages and shortcomings of both the Bank of New-York and his own land-bank proposal in the weeks when both were being considered before the legislature.

Even writing under a cloak of anonymity, Livingston’s harshest criticisms of the Bank of New-York addressed only the propriety of having merchants serve as bank directors. In the process of pointing this out, Livingston showed that he envisioned a significant public role for his proposed land bank. The land bank, he said, could someday hold state government deposits, something that likely would enable it to multiply the amount of credit it offered to its clients. This prompted the chancellor to ask whether “the Government [could] lodge their money with those who afford them no security but their good characters” in a commercial bank. Could a “careful Guardian leave the money of his Ward with a Bank whose Directors must change every year,” especially when it “circulates more than its capital” and its credit “depend[ed] on the opinion the world entertain of Directors who, from being in trade, are always liable to strong temptations to aid each other?” He warned that the temptations of banking would drive some “Merchants [to] change their profession and become Stockholders.” Merchants, he argued, could not be trusted to oversee a stable and publicly useful bank.62

Both bank cohorts, then, recognized that the petitioning and charter-application process was a dynamic one. Although they did not consider combining their proposals, both offered compromises to attract new supporters and build a more persuasive case for incorporation. The petitioning process therefore not only aggregated financial capital but also encouraged the consolidation of human and political capital as well. Both bank coalitions assumed that the legislature would approve at least one bank petition in 1784. The only question seemed to be which one would clear the hurdle.

The Legislature

Within the legislature, however, that question was far less clear-cut.

As bank partisans offered concessions to each other in the hopes of building consensus around dueling proposals, state legislators—the audience for these petitions—seemed increasingly unwilling to take affirmative steps on behalf of either bank.

Despite the connections that the Bank of New-York enjoyed in the legislature, there remained twelve senators and sixty-eight assemblymen in the legislature who were not directly linked to the proposed bank. New laws had to win majority support not only in both houses, but also in the state’s Council of Revision—a panel composed of the governor, two justices of the state’s supreme court, and the state’s chancellor, who happened to be Robert R. Livingston, the chief supporter of the rival land bank. Only after winning support in the Council of Revision could a bill be laid before the governor for his signature, making it necessary for the promoters of both the commercial Bank of New-York and the land Bank of the State of New York to lobby legislators using a variety of appeals—neither bank was large enough, after all, to give every lawmaker a line of credit or a seat on its board of directors.

Harnessed from across the state and crammed into the narrow quarters of City Hall, New York’s state legislature reflected many of the same tensions and motivations found in the civic and economic lives of the few dozen city blocks that surrounded them near the southern tip of Manhattan. Any person capable of reading a newspaper or entering a tavern was acutely aware of the divisions between loyalist Tories and patriotic Whigs in the city, and vehement anti-Tory passions were expressed by legislators who proposed to strip former Loyalists of their rights to hold office, vote, or own property. A cadre led by Albany County state senator Abraham Yates was hostile even to the notion of reconciliation with Tories and relished questioning the patriotic credentials of Whigs who dared to socialize or do business with onetime Loyalists. One of Robert Livingston’s friends believed that the “narrowness of [Yates’s] mind & the badness of his heart … injures this state more than ever his services will expiate.” “Men of integrity & education,” he fumed, indulged Yates’s “pretended patriotism” and “suffer that old booby to thwart & disconcert whatever has the appearance of wise & sound policy with impunity.”63

The Bank of New-York steered directly into this storm once it published the roster of its managers and directors in city newspapers, making it a target for anti-Tory politicians and their allies. A letter to a New York paper soon wondered what was behind the “present confidence and audacity” of “truly detestable and obnoxious Tories” who appeared in public as bank directors. The Whig directors and bank president McDougall, one writer asserted, had become nothing more than “advocates” for these “bloody-minded villains,” and it was “high time” for the state legislature to once and for all “make a proper discrimination” between “friends and foes of this country” by banishing “sworn enemies” who “endanger the piece of society by parties, factions, and cabals.” The Bank of New-York, the writer concluded, was nothing more than an “absurd and ridiculous system” for advancing Tory interests.64